A valuation matters when it can be reviewed

For unlisted shares, the reference value is not a standalone estimate. Your accountant or auditor needs to trace the source data, normalizations and method so the file holds up during a transfer or review.

The rules allow a valuation by a certified accountant or auditor within the provided window. Without an audit trail, a report becomes a weak spot rather than evidence.

Role

What your accountant or auditor needs to review

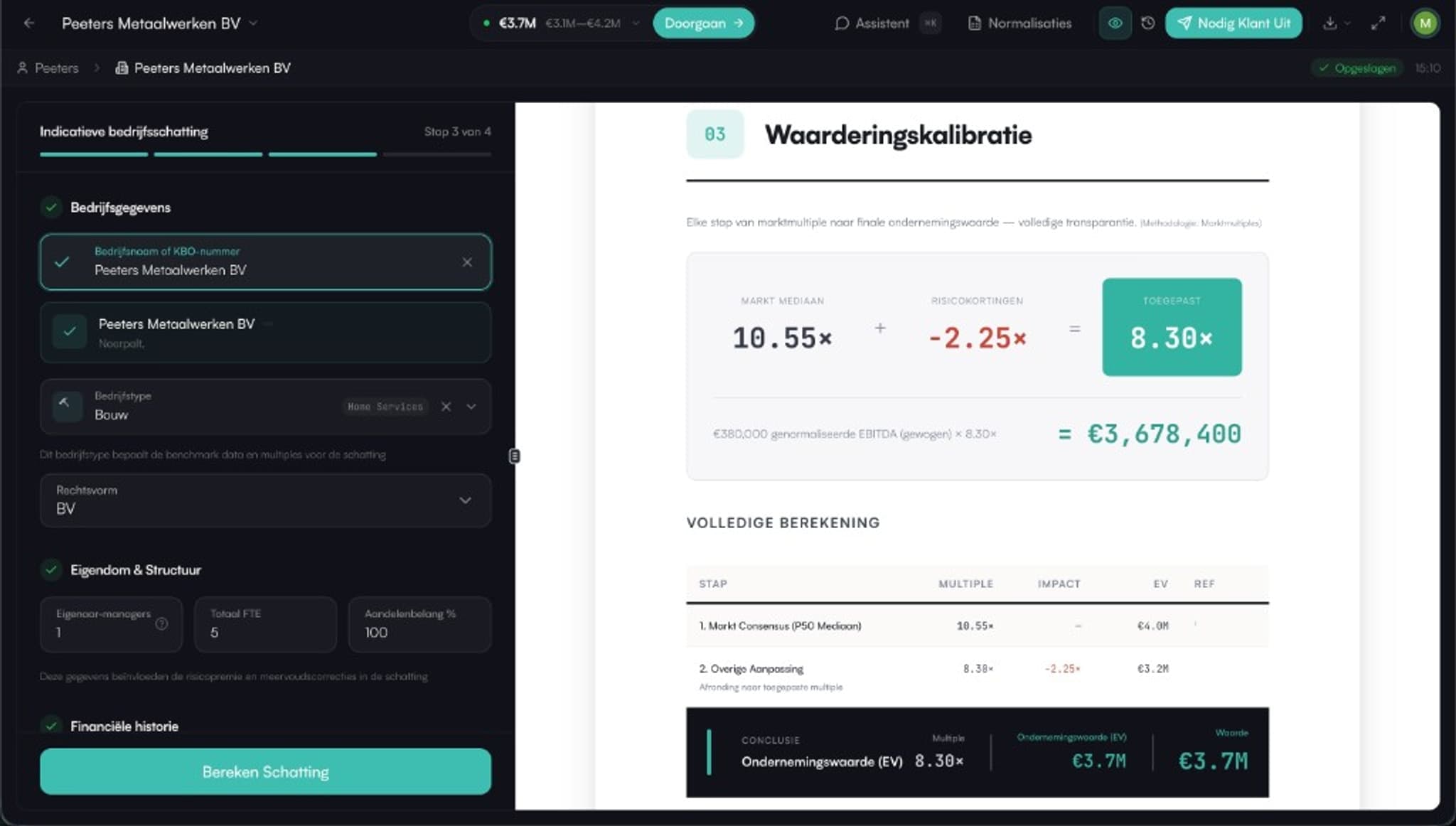

A defensible valuation file starts with traceable figures: annual accounts, interim results, normalizations, debt, cash, exceptional costs and the chosen methods.

The accountant or auditor does not only look at the output. They look at the path to it: which assumptions, which normalized EBITDA, which method gets weight, and why.

- Source data and company identity need to be traceable

- Normalizations need to be transparent and repeatable

- Methods and weightings need to be explainable to a third party

Workflow

Upswitch makes the file reviewable

Upswitch bundles valuation methods, normalizations and reporting in one workflow. The owner gets speed, and the advisor gets a file they can review, adjust and preserve.

That turns the reference value from a black box into a substantiated starting point for tax discussion, transfer planning or family planning.

Frequently asked questions

Does an accountant need to make the valuation?

For unlisted shares, a valuation by a certified accountant or auditor can be relevant within the provided window. Discuss formal requirements with your adviser.

What makes a report defensible?

Traceable data, transparent normalizations, multiple methods, clear assumptions and an audit trail an accountant or auditor can review.

Can my accountant work with Upswitch?

Yes. The workflow is designed so an accountant can review the file, refine assumptions and discuss the report with the client.

Make your valuation reviewable

Start with a substantiated report and involve your accountant before the tax window closes.

This page provides general information and is not tax, legal or audit advice. Have the formal requirements for your valuation file confirmed by your accountant, auditor or tax adviser.

Related depth and references

Related depth and references

Capital gains tax 2026: overview

Back to the overview: the law, lump-sum vs. professional, and how Upswitch helps.

Reference value 31 December 2025

Why the reference moment drives your later gain.

Substantial shareholding rates

20% threshold, €1M exemption and progressive brackets.

Lump-sum vs. professional valuation

Book equity + 4× EBITDA versus ten methods.

Deadline 31 December 2027

The window to lock in your valuation in time.

Lump-sum vs. professional

Why method, normalization and audit trail matter.

Deadline 31 December 2027

The window to formally lock in your valuation.