A 20% holding changes the calculation

When the transferor holds at least 20% of the rights in the company being transferred, the substantial-shareholding regime may apply. It has a higher exemption, but also its own filing and valuation risks.

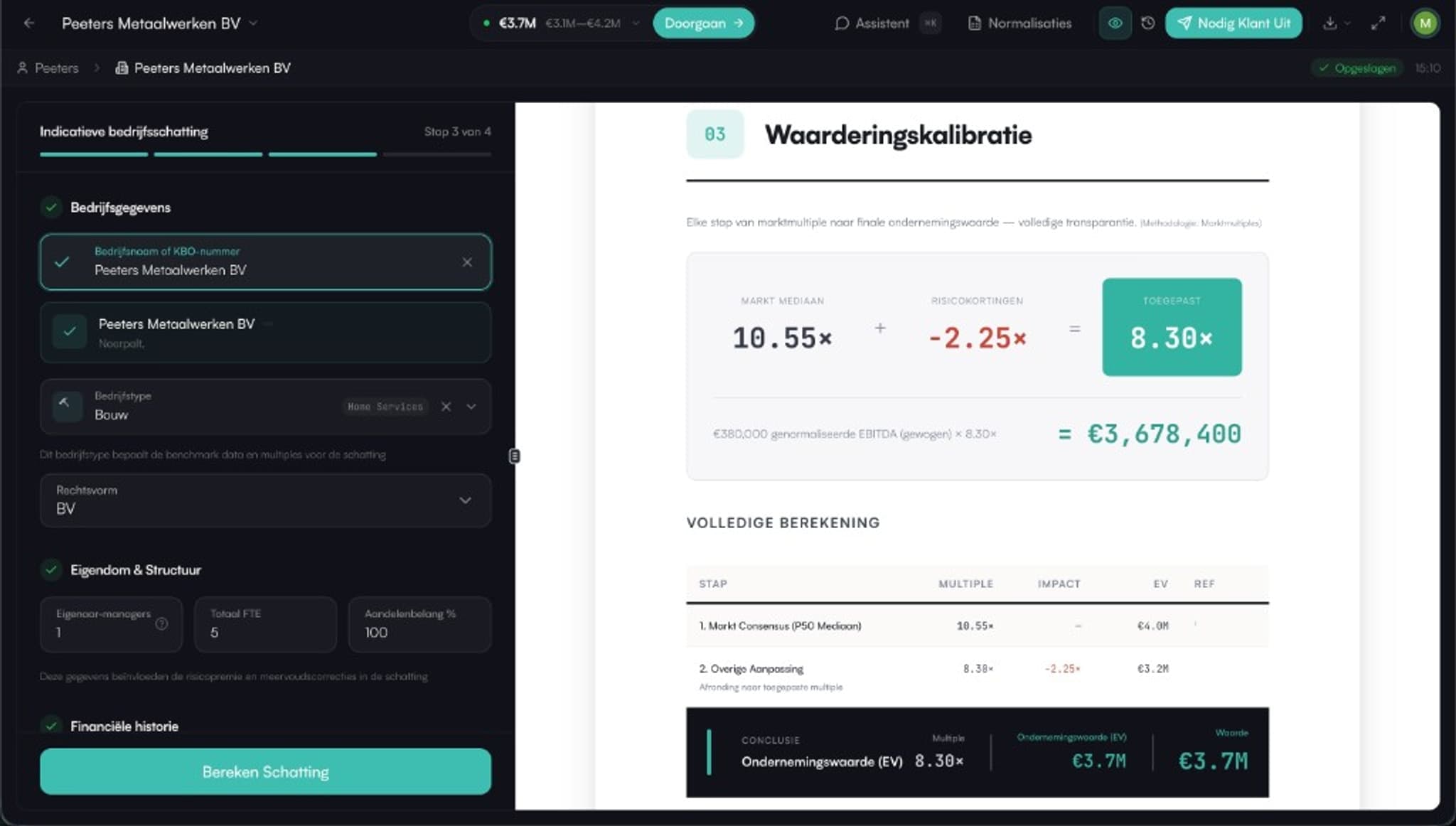

The first €1,000,000 of gains may be exempt over five years. Above that, progressive brackets from 1.25% to 10% can apply depending on the size and context of the transfer.

Threshold

When the substantial-shareholding regime applies

The regime targets shareholders who hold at least 20% of the rights in the company at the time of transfer. The threshold is generally assessed per shareholder, not automatically at family level.

For founders, holdings and family shareholders, this is often the most relevant category. A sale to a non-EEA buyer or an internal capital gain can be treated differently, so confirm the classification.

- Threshold: at least 20% of the rights in the company

- Exemption: first €1,000,000 of gains over five years

- Progressive brackets: 1.25%, 2.5%, 5% and 10%

Valuation

The reference value remains the starting point

Even under the substantial-shareholding regime, the tax focuses on gains that arise after 31 December 2025. A defensible value at that reference date determines how much of a later sale price becomes taxable.

A low or poorly documented value creates room for dispute. A professional report gives your accountant or auditor the data, normalizations and methods needed to substantiate the starting point.

Frequently asked questions

What is a substantial shareholding?

In this context, it generally means holding at least 20% of the rights in the company whose shares are transferred. Always confirm the exact classification with your accountant.

Is the first €1 million always exempt?

The special exemption is assessed over five years and depends on the concrete transfer category. It does not work like the general annual exemption.

Why do I still need a valuation?

Because historical gains up to and including 31 December 2025 remain outside the new tax. The value on that date is your defensible starting point.

Prepare your 20% file

Start with a substantiated reference value and let your accountant confirm the tax treatment.

This page provides general information about the substantial-shareholding regime and is not tax or legal advice. Thresholds, rates, exemptions and filing duties depend on your situation: confirm them with your accountant or tax adviser.

Related depth and references

Related depth and references

Capital gains tax 2026: overview

Back to the overview: the law, lump-sum vs. professional, and how Upswitch helps.

Reference value 31 December 2025

Why the reference moment drives your later gain.

Lump-sum vs. professional valuation

Book equity + 4× EBITDA versus ten methods.

Role of accountant and auditor

Why reviewable data and normalizations matter.

Deadline 31 December 2027

The window to lock in your valuation in time.

Reference value 31 December 2025

Why the tax starting point determines your later gain.

Lump-sum vs. professional

Why a defensible valuation is stronger than a lump-sum fallback.